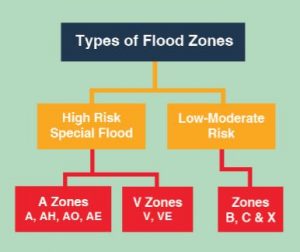

A and V zones are high risk flood areas, and you are required to carry flood insurance. B, C, and X zones are lower risk but it is recommended you purchase flood insurance, as nearly 25% of flood claims come from low risk areas.

A and V zones are high risk flood areas, and you are required to carry flood insurance. B, C, and X zones are lower risk but it is recommended you purchase flood insurance, as nearly 25% of flood claims come from low risk areas.